Digital Disruption & Artificial Intelligence (AI) is one of five thematic mega forces[1] tracked by the BlackRock Investment Institute, which has predicted that the technologies are poised to dramatically alter the supply-demand balance across multiple business sectors.

Markets currently underestimate the full extent of this revolution, according to the Institute, BlackRock’s investment research arm. This is particularly true for the infrastructure needed to operate AI: data centers and semiconductors, and the vast energy required to run the systems. For the latter, the impact will be felt on the key transition metal that is copper. BlackRock oversees one of the world’s largest pools of thematic investment portfolios.

To discuss more about these topics, we caught up with Omar Moufti, Thematics & Sectors Product Strategist at BlackRock’s iShares unit. STOXX and BlackRock collaborated in the 2023 launch of the iShares Copper Miners UCITS ETF, and more recently the two companies worked on the introduction of two funds targeting opportunities in AI: the iShares AI Infrastructure UCITS ETF and the iShares AI Adopters & Applications UCITS ETF.

Omar, BlackRock has referred to AI as an “industrial revolution” that is propelling a historic capital expenditure cycle. Can you develop on that?

“Since 2023, we’ve witnessed the vast reach of AI. This technology has transcended buzzword status and is rapidly being integrated across the global economy, permeating day-to-day operations with real-world outcomes, and transforming entire industries in the process.

Today, the most compelling opportunity in AI may lie less in the digital realm and more in the physical infrastructure that enables it: hardware, digital networks and power systems.

Virtually all paths of greater AI adoption are set to accelerate demand for the ‘picks and shovels’ behind AI. As we integrate new AI applications, power high-performance computing and continue to populate the cloud, we will need evolved chips and data centers that can sustain ultrafast network connections. BlackRock’s Fundamental Equities team estimates that AI servers cost roughly 40 times more than the traditional data centers of the past. As a result, technology giants and other investors are set to devote more than USD 1 trillion on AI capital expenditure in the next couple of years, according to some estimates.[2]

The scale of the infrastructure build-out required to run the real estate, computing power and data storage that will support AI’s growth has little or no precedent in modern times. In that sense, AI represents not just a technological leap but the dawn of a new industrial revolution.”

So how do you position a portfolio to capture the beneficiaries of this transformation?

“There are plenty of potential beneficiaries of this historic capital expenditure cycle — ranging from operators and suppliers of data centers, to chipmakers, as well as suppliers of electric power infrastructure and critical materials. We view AI as a specific mega force investment theme, but getting granular may be the most efficient way to unlock its full potential.

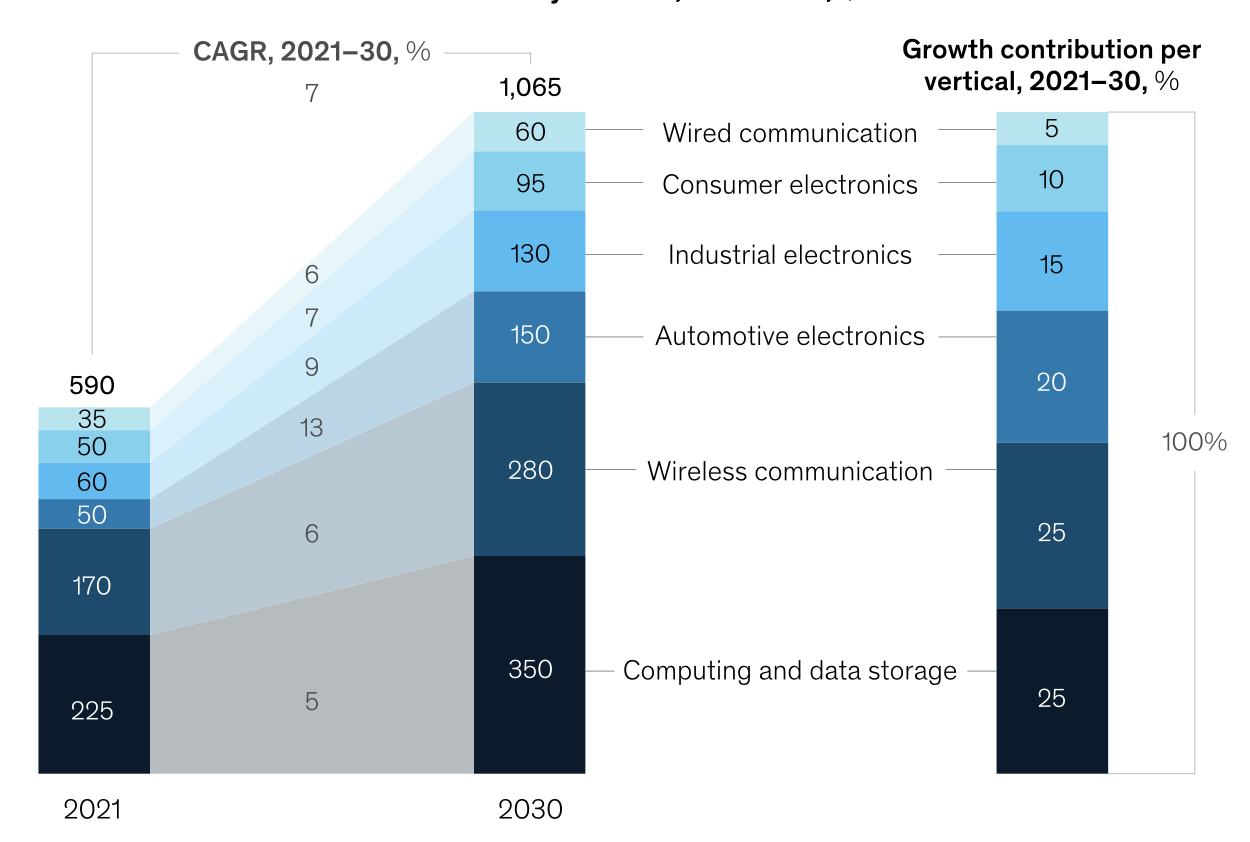

The market has primarily focused on semiconductor companies and specifically on Graphics Processing Units (GPUs), but the AI opportunity is much bigger than that. The chip industry is projected to top USD 1 trillion in revenue by 2030, with computing and data storage driving 25% net growth (Figure 1).[3]

When constructing a portfolio of AI beneficiaries, it is important to identify companies across all sectors whose revenues are poised for a paradigm shift in this investment cycle.”

Figure 1: Global semiconductor market value by vertical, indicative. USD billions.

AI is a rapidly developing technology. How do you make sure you can accurately capture its “winners” in such a fast-moving landscape?

“Revenues are a tangible and transparent factor upon which to implement an investment strategy. Many companies are already reporting strong revenue trends — be it actual sales or guidance — which informs us who will benefit from this upswing.

That said, AI technologies call for keeping an eye on the future, identifying those companies whose products and services will lead innovation in the years ahead. A powerful tool at hand is the analysis of patents, which are forward-looking IP documents that can be processed in a systematic manner. A company with significant patent activity in a certain technology today is likely to develop and commercialize related products in the future, more so than a competitor with little or no current patent exposure.”

BlackRock has also highlighted copper as a related area of growth. What role does the commodity play in this AI cycle?

“Power infrastructure will need a fundamental overhaul to meet soaring AI energy demand. Data centers need plenty and affordable electricity to run and cool high-performance servers.

Critical IT power refers to the usable electrical capacity available to servers and networking equipment within a data center’s server racks. In the US alone, this capacity will need to triple from 2023 to 2027, and rise well beyond, to keep pace with the accelerating demand driven by AI’s expansion.

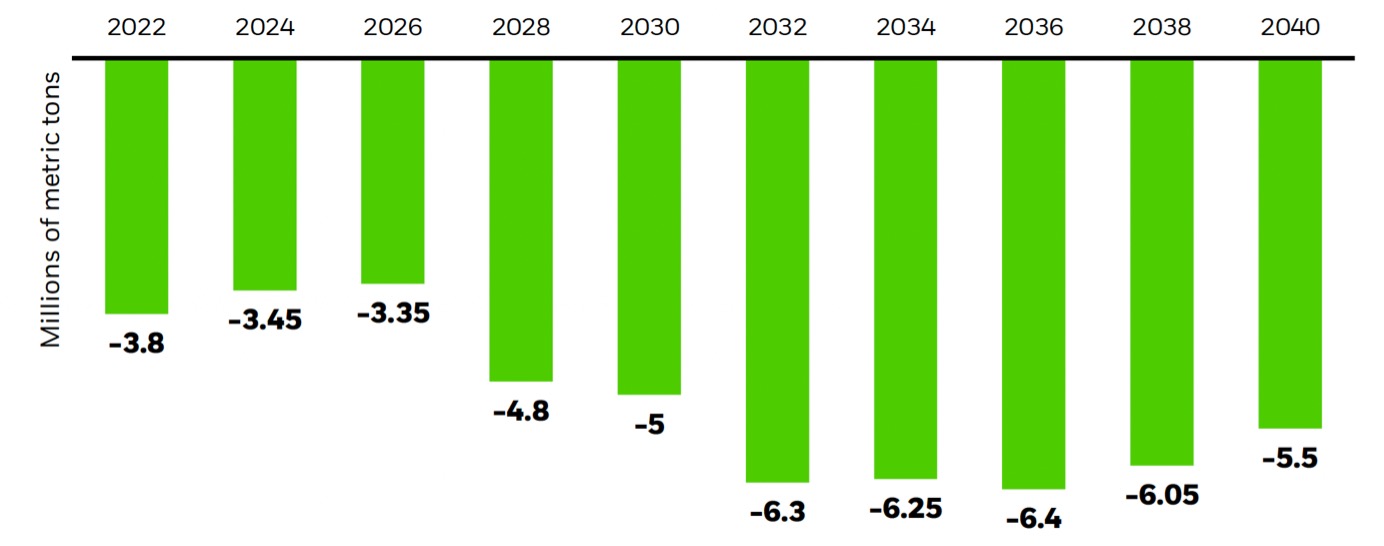

This means an exponential amount of energy will be required at a time when efforts to transition towards net-zero objectives is depleting supplies of copper. The metal is a key material across the entire chain of the electricity grid, including conductor lines, cables, transformers and circuit breakers. Power grids are already competing with factories, electric vehicles, electronics and clean energy applications for copper.

BloombergNEF has forecast that demand for the red metal will increase by over 50% between 2021 and 2040, with supply falling far short. It takes an average of 10 to 20 years to develop a new copper mine, a lengthy process that exacerbates the shortage. Persistent copper supply deficits could become a chokepoint for AI’s expansion.”

Figure 2: Forecast supply deficit, refined copper

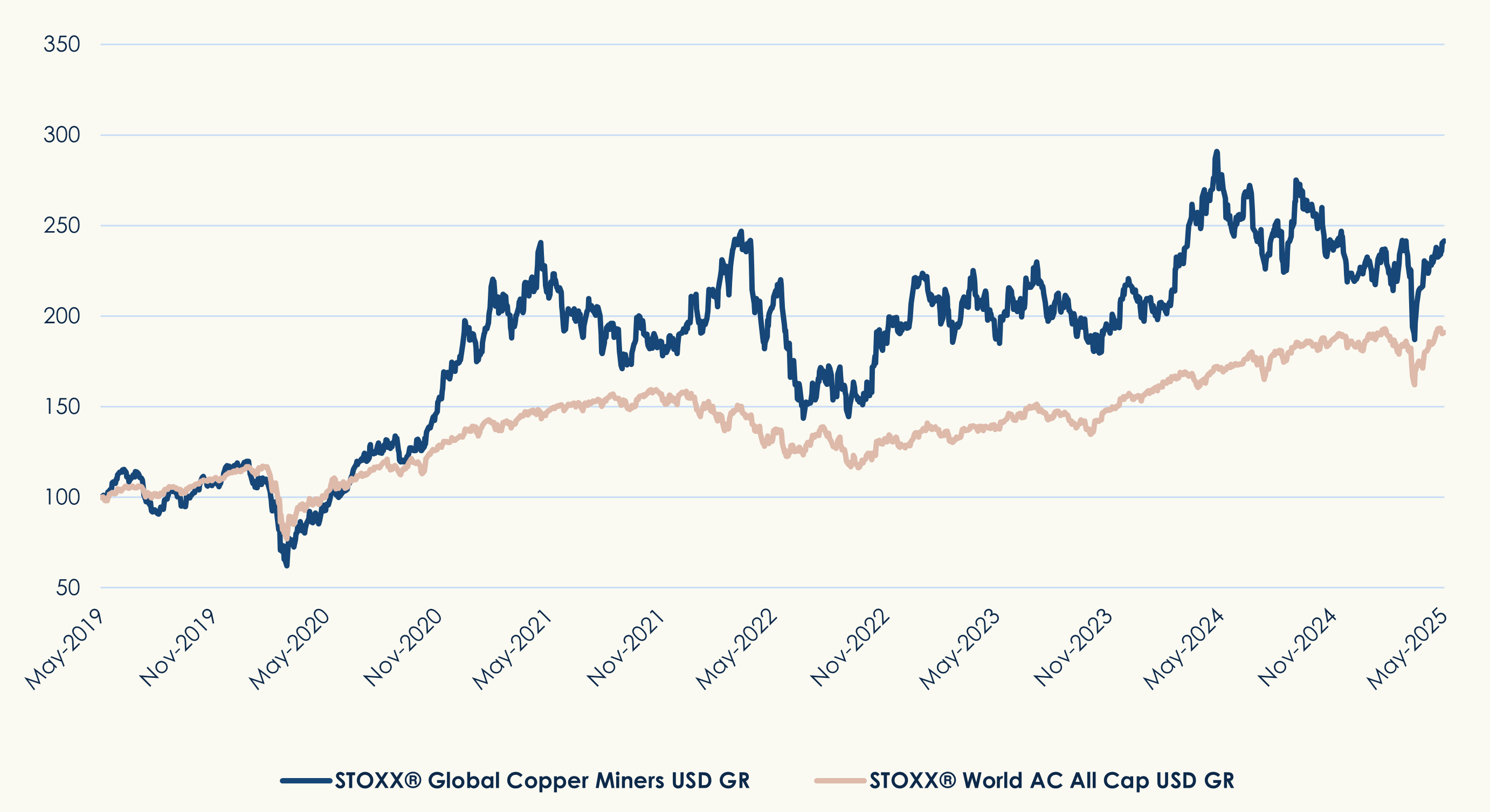

What’s in the iShares Copper Miners UCITS ETF and its underlying, the STOXX® Global Copper Miners index?

“The STOXX Global Copper Miners index is comprised of companies with significant exposure to the copper mining industry, whether through revenue share or market presence. As such, the index captures the specialized miners as well as global, diversified companies with important copper businesses.

The index has done very well since the COVID pandemic, as investors react to the multi-year glut in supply and projected increase in base prices. It underperformed global equities in 2024, but has rebounded this year. In the past six years, the index has risen by 141%, compared with 91% for the STOXX® World AC All Cap benchmark.”

Figure 3: STOXX Global Copper Miners index performance

Finally, what does a thematic investing approach offer when targeting these megatrends, that a sector-based fund doesn’t?

“Thematic mega forces transcend traditional industry and sector classifications. They are universal, long-term trends that impact a wide range of businesses in ways that differ from typical economic cycles. Sector-based funds are not designed to tackle such broad themes, and they may provide exposure to segments that don’t directly benefit from the theme in focus. A technology fund may not offer the nuanced view to harness the full AI value chain, while a broad basic-materials index may not allow a targeted investment in copper miners.

Thematic investing is a way of seeing the world, identifying changes that are yet to fully materialize and trying to capture those changes in a holistic manner.”

[1] BlackRock strategists currently consider five “mega forces” which can guide thematic investing. These five forces are big, structural changes that are shaping macroeconomic trends and market volatility, and affect investing. They are Digital disruption and artificial intelligence, Geopolitical fragmentation and economic competition, Future of finance, Demographic divergence and Transition to a low-carbon economy.

[2] Goldman Sachs Global Macro Research, “Gen AI: Too Much Spend, Too Little Benefit?” June 25, 2024.

[3] Source: McKinsey & Co. “The semiconductor decade: A trillion-dollar industry,” April 1, 2022.