European energy companies — whose shares just posted their best quarter in more than 15 years even as Middle East tensions weighed on most other sectors — may face a windfall tax on their oil price gains.

Economy and finance ministers from Austria, Germany, Italy, Portugal and Spain have asked the European Union to tax energy companies’ surplus profits to alleviate the burden on consumers caused by rising fuel prices, according to reports.[1] Electricity will be taxed at a lower rate than fossil fuels across the bloc under a bill that the European Commission (EC) is poised to unveil next month, Politico reported separately.[2]

Brent crude topped USD 110 a barrel in March after Iran blocked tanker traffic through the Strait of Hormuz in retaliation for US and Israeli military strikes on February 28. Oil prices have fluctuated in April as traders assess a temporary ceasefire, but Morgan Stanley estimates Brent will average USD 80–90 per barrel in 2026 even if tensions ease — well above the USD 60 forecast the bank’s analysts made last November.[3]Analysts have boosted their first-quarter earnings estimates for STOXX Europe 600 energy companies by 18% since the end of February, according to a BofA analysis.[4]

The five European countries want to revive and boost a mechanism that taxed roughly EUR 28 billion on excess fossil fuel profits during the post-Ukraine war price spike, Euronews reported. The EC is considering the proposal, the news agency said.[5]

Stocks rally

The STOXX® Europe 600 Energy index added 37.2%[6] in euros over the first three months of 2026, its best start to a year and widest outperformance relative to the STOXX® Europe 600 benchmark — which fell 0.9% in the quarter — in data going back to 2010. Crude prices jumped 79% over the three months as the US-Iran conflict disrupted supply in the strategic Persian Gulf region.

The STOXX® Global 1800 Energy index, meanwhile, added 35.5% in dollars in the first quarter, outperforming its benchmark by 38.7 percentage points, also posting its best quarter since at least 2010.

Gains in energy equities came even as most other sectors struggled, and traders reassessed expectations for inflation and interest rates, reversing earlier forecasts that many central banks would cut borrowing costs this year. The International Monetary Fund on April 14 cut its global growth forecast, citing higher oil prices.[7]

A decade of mixed performance

European oil stocks were frequent underperformers in the past decade — lagging the market in seven of the ten calendar years from 2015 through 2024.

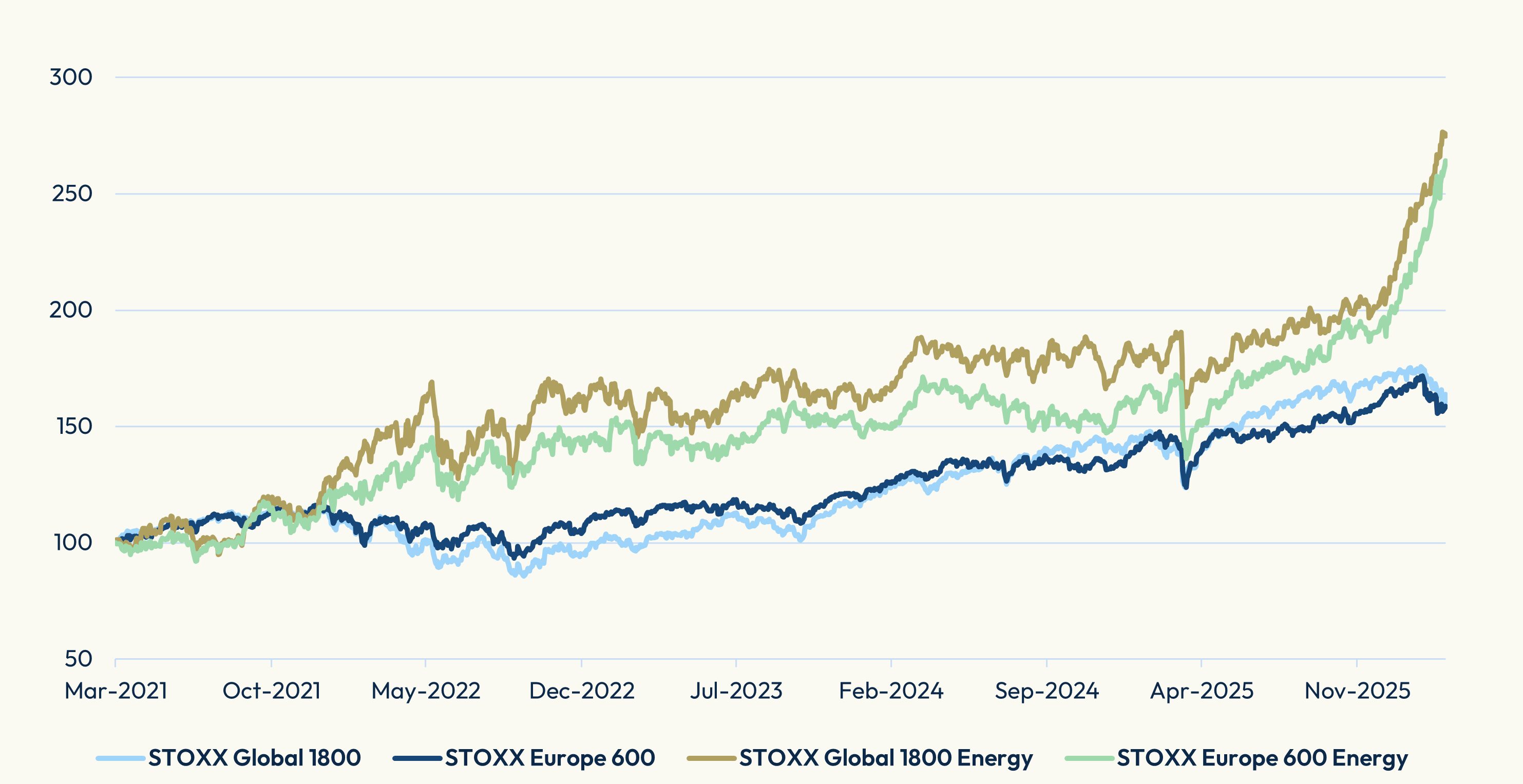

Figure 1 shows the five-year performance of European and global energy stocks against the STOXX Europe 600 and STOXX® Global 1800 benchmarks. Oil stocks had a very strong 2022 in absolute and relative terms, but lost ground over the following two years. In 2026, the sector has diverged positively from the broader market, the chart shows.

Figure 1: Index performance

Trading activity

Rising oil and share prices have triggered a flurry of trading activity in energy-related products. The number of futures on the STOXX® Europe 600 Oil & Gas index traded on Eurex rose 39% in March relative to the year-earlier period, while options on the index jumped 276% year-on-year. The iShares STOXX Europe 600 Oil & Gas ETF attracted EUR 110 million in net flows in March, taking the investments this year to EUR 170 million, according to STOXX data. The Amundi STOXX Europe 600 Energy ESG Screened UCITS and Invesco STOXX Europe 600 Optimised Oil & Gas UCITS ETFs also received inflows in March.

Even after the recent rally, energy stocks remain cheaper than the benchmark. The STOXX Europe 600 Energy traded at 12.8 times expected earnings at the end of March, compared with a multiple of 15 for the STOXX Europe 600, according to STOXX data.

Shrinking sector weight

The surge in energy stocks may not be benefiting portfolios as much as it once would have. The sector has lost its influence in markets as other industries grew faster and climate-related mandates led many investors to shed oil stocks.

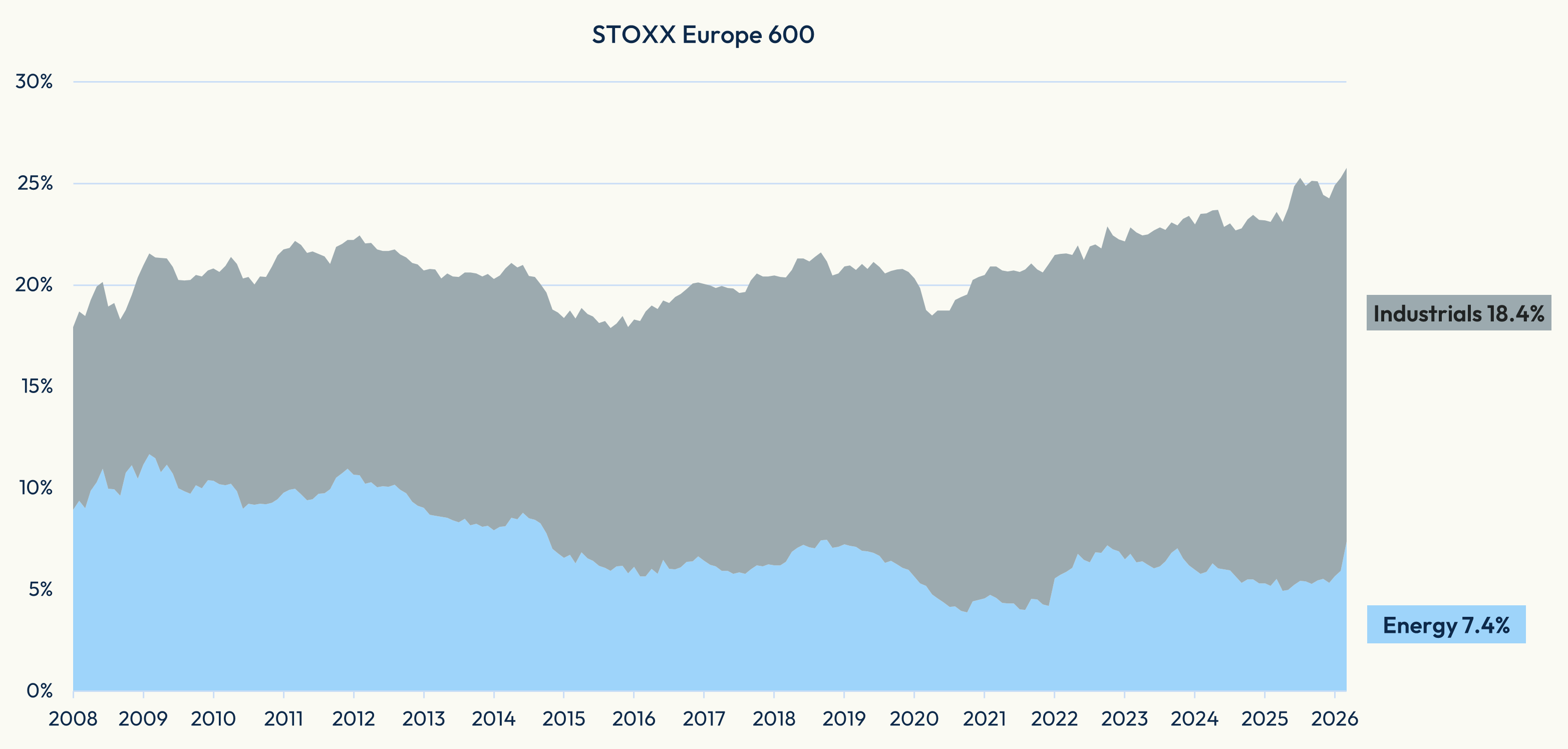

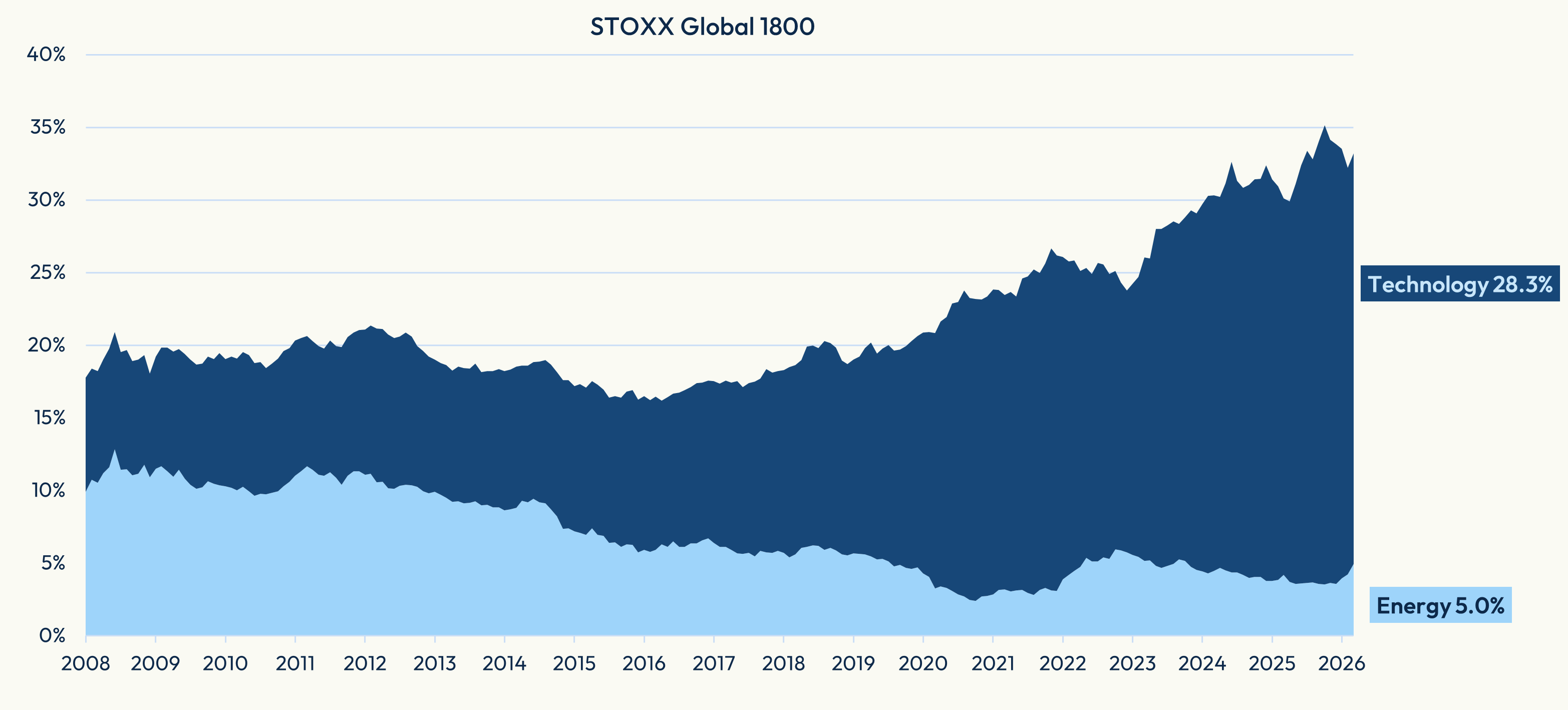

Figure 2 shows the historical weighting of the Energy Supersector in the STOXX Europe 600 and STOXX Global 1800 benchmarks.

Energy stocks made up 5.3% of the STOXX Europe 600 at the end of last year, down from a period peak of 11.7% in February 2009. Over the same period, Industrials recorded the largest gain in sector weighting.

The relevance of energy stocks in the STOXX Global 1800 index has fallen even more — from as high as 12.8% in June 2008 to 3.6% at the end of 2025. By contrast, Technology stocks rose from 8.1% of the global benchmark to 30.3% over the same period.

Figure 2: Share of oil stocks in benchmarks

Closing underweights

Investors have been underexposed to energy stocks for some time. According to the Wall Street Journal, which cited data from State Street Investment Management, energy-sector ETFs have seen net outflows since 2021, compared with net inflows for all other sectors.[8]

That stance may explain the strong inflows into the sector in 2025, which likely reflect investors closing underweight and short positions. Energy stocks have emerged as a natural hedge against the year’s defining geopolitical risk — a widening Middle East conflict — and its twin consequences: disrupted global oil supplies and renewed upward pressure on interest rates.

[1] Euronews, ‘Five EU ministers call for new windfall tax on energy profits amid price surge,’ April 4, 2026.

[2] Politico, ‘Fossil fuels face higher taxes than electricity under looming bill,’ April 14, 2026.

[3] Morgan Stanley Research, ‘Iran Conflict: Three Scenarios for Markets,’ April 7, 2026.

[4] BofA Securities, ‘European Earnings Season,’ April 9, 2026.

[5] Euronews, ‘EU considering excessive profit taxes on oil and gas companies, foreign profits remain unclear,’ April 10, 2026.

[6] All indices display gross returns.

[7] Reuters, ‘IMF cuts growth outlook, warns world already drifting toward more adverse scenario,’ April 14, 2027.

[8] WSJ, ‘Energy Stocks Are Having a Moment That Could Last,’ April 7, 2026.