Factor investing has become ‘smarter’ in recent years, with indices allowing enhanced strategies that accommodate robust definitions and optimized methodologies that can control for risk and calibrate exposures.

To discuss these developments, Legal & General (L&G)[1] and STOXX recently hosted a webinar that focused on factor efficacy, innovation in index design and the interplay with sustainability objectives.

The webinar featured Fadi Zaher, Head of Index Solutions at L&G, and Arun Singhal, Head of Product Management at STOXX. The discussion was moderated by Stefan Bilby, Head of Index Distribution at L&G.

Multifactor strategies can help mitigate factors’ cyclicality

Fadi kicked off the discussion by explaining the history of factor investing and how we arrived at the modern and exact factor definitions of today.

“When we talk about data, it’s important that you have enough history to understand how factors perform in different markets and different cycles,” Fadi said, adding that L&G and STOXX focus on factors that have been tested over time “and tend to stay.”

That data, and technological advances, have underpinned the factor journey, Arun explained, while research and years of experience have helped shape factor portfolios that can overcome inherent problems of factor investing such as unwanted biases or cyclicality.

“There is extreme short-term cyclicality at the individual factor level,” Arun said. “So, the question is, how do you build a multifactor portfolio to harvest the premia that you see over the long term, but you don’t feel the short-term cyclicality of single factors?”

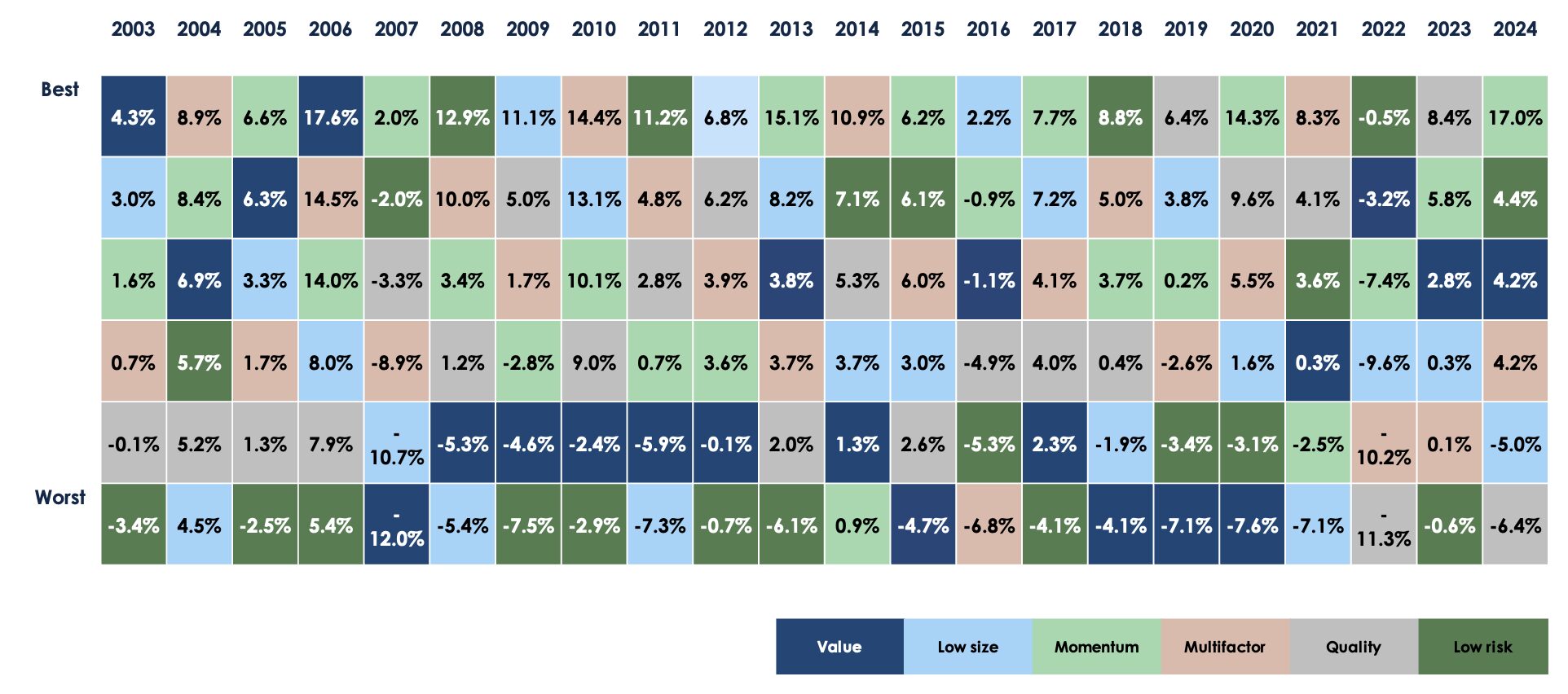

Figure 1 displays, from top to bottom, the best- to worst-performing factors in Europe each year. As the chart shows, there is a high shift in performance of single factors from year to year.

Figure 1: Active returns of STOXX European factor indices

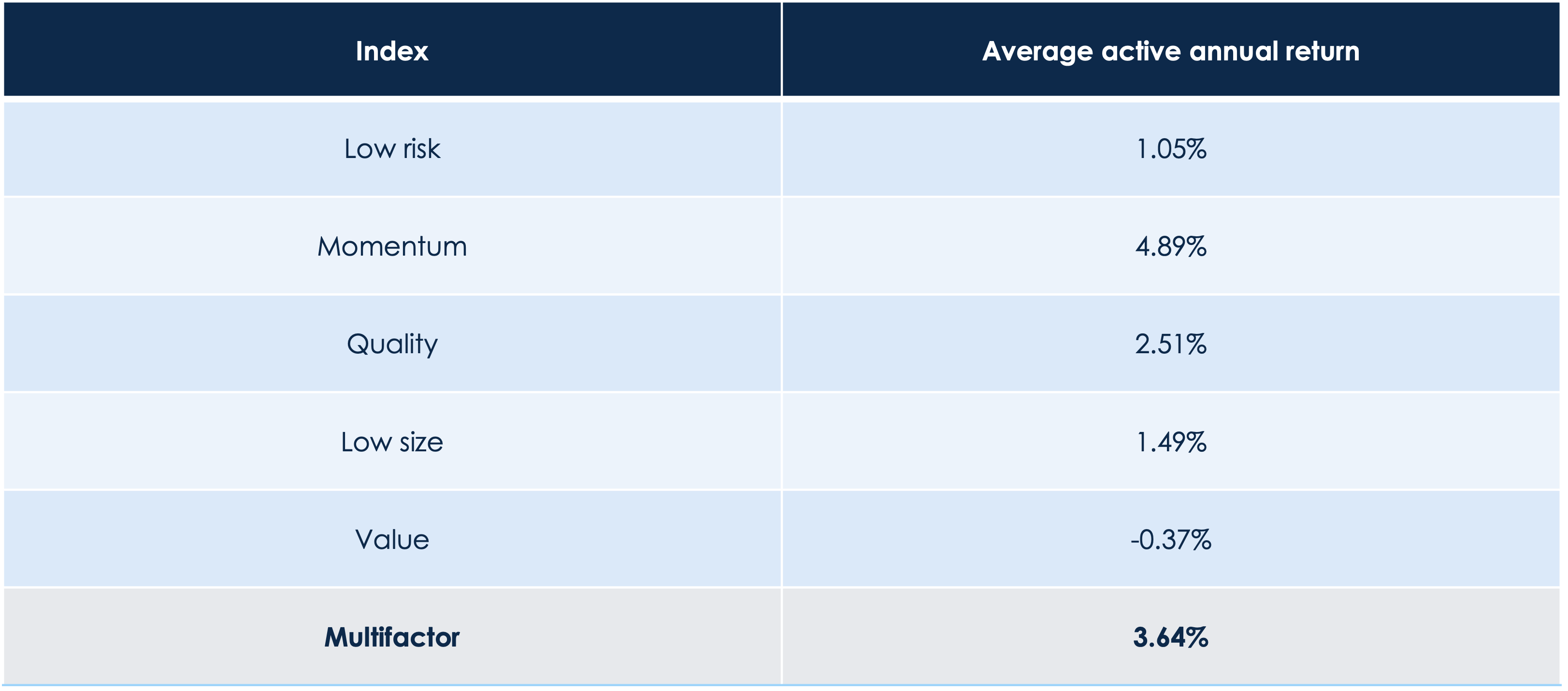

A multifactor strategy can smooth out that cyclicality by avoiding allocating too much weight on any single factor, Arun explained. In fact, Multifactor as a signal has shown the highest annual active returns in STOXX’s factor suite in data going back to 2002, after Momentum (Figure 2).

Figure 2: Average active annual returns – Europe

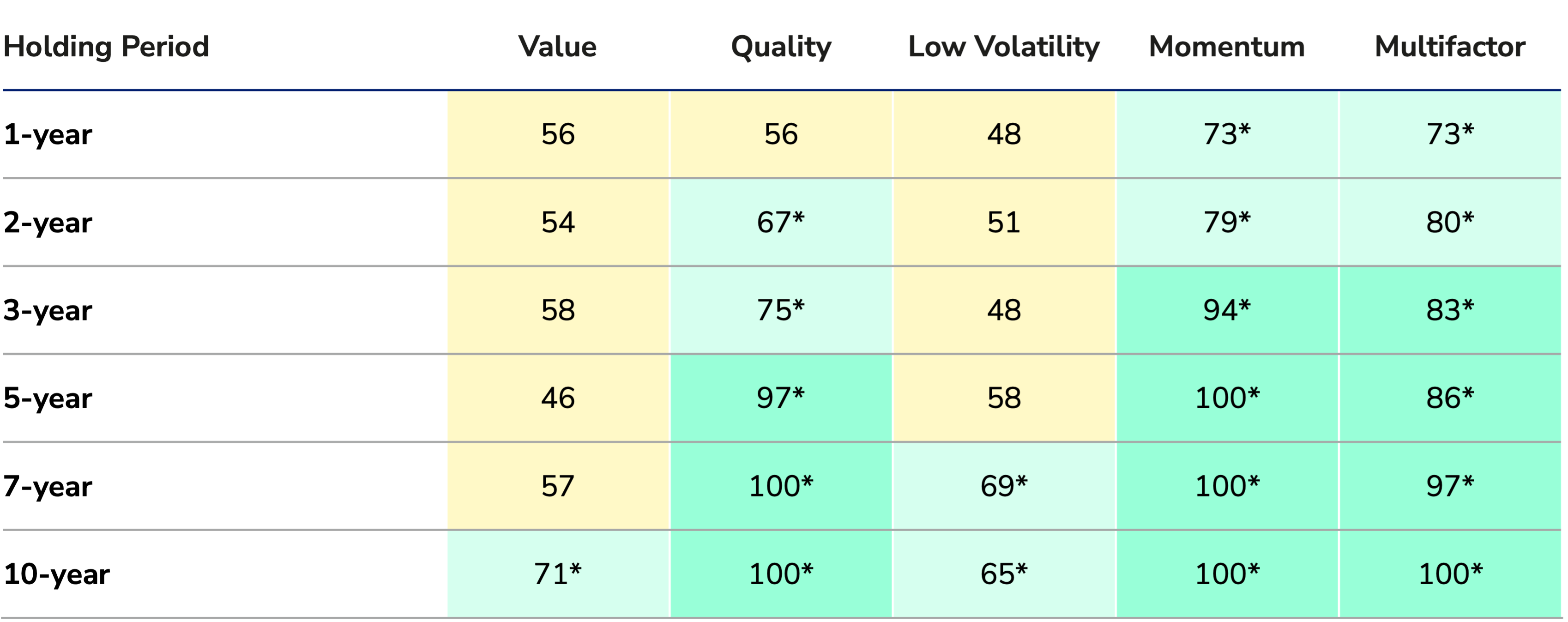

To prove the point of short-term cyclicality but long-term outperformance, Fadi presented the table in Figure 3, which displays the efficacy of factor signals across time periods. The hit-rate number shows the percentage of instances in defined rolling periods over 22 years where each factor strategy beat the market.

“The further you go down in time, the more likely that you are going to outperform the market,” Fadi said. “Even more interestingly, when you look at Multifactor, these probabilities work across different time horizons.”

Figure 3: Short-term cyclicality but long-term outperformance — Hit rate %

How index design has evolved to capture factor premia

Index construction is vital in reflecting factor evolution and maximizing outcomes, Arun said. Today, a factor portfolio is composed of the targeted factor(s), while additional considerations include sector, stocks and region exposure; and built-in constraints including risk control, weights and tilts — all often optimized via a risk model. Finally, there are sustainability filters and overlays, a topic to which the webinar devoted its entire final chapter.

“There are numerous variables and numerous decision points that you want to take into account” in building a factor portfolio, Arun said.

He explained that STOXX factor index construction focuses on robustness, clarity and investability. That includes tested and institutionally accepted factors; strong exposures with controls of unintended factor biases and ex-ante tracking errors; and constraints around liquidity, turnover and number of stocks.

Interplay between sustainability criteria, climate considerations and investment styles

A main feature of factor portfolio design today is that strategies must now incorporate three dimensions: the traditional risk and return, plus sustainability impact as a more recent addition, the panel said. This is in response to increasing demand from institutional and retail investors, who wish to incorporate responsible investing practices into a systematic factor-based approach.

Fadi presented the case study of a factor portfolio that improved its sustainability score and significantly reduced the carbon footprint, without deviating too much from a benchmark.

“You can actually achieve meaningful excess returns of factor premia with even a small tracking error, and that’s a well-designed, balanced strategy that can capture both the sustainability feature and the investment objective,” he said.

The iSTOXX L&G multi- and single-factor ESG suite of indices, the result of extensive collaboration between STOXX and L&G, blend index optimization techniques and incorporate L&G’s proprietary factor and ESG scores, as well as their Future World Protection List (FWPL) exclusions.

Learn more

Factor investing is gathering interest amid record inflows into European equities this year. In that sense, the webinar may prove both enlightening and timely. You can watch the full recording here.

[1] Legal & General’s asset management business is a major global investor across public and private markets, with GBP 1.1 trillion in assets under management as of the end of 2024.