STOXX attended SP Intelligence Europe 2026 on May 21, an event bringing together the structured products community, represented by Tom Shuttlewood, Head of Strategy & Digital Indices, Product Development.

Tom presented on downside protection and quantitative investment strategies (QIS) — a timely topic given the continued evolution of indexing products designed to provide various forms of market insurance, and a volatile geopolitical environment.

We caught up with Tom after the event to discuss these topics in more depth. Below is our exchange.

Tom, can you explain how market participants are turning to indices to obtain downside protection?

“Indexing has changed quite dramatically over the last 25 years. We started with broad market beta, then moved into alpha, smart beta and risk premia — bringing more sophisticated ideas around low-volatility portfolios, risk-off factors and alternative weighting schemes.

Then came customized quantitative solutions, or QIS: tailored strategies for specific risk appetites, managed volatility measures, dynamic allocations and derivative overlays for capital preservation. Many of these strategies have an emphasis on downside protection, and this is an area that continues to grow strongly.

If I were to categorize these approaches, I’d say I see three broad buckets:

- dynamic risk mitigation,

- dynamic diversification and

- pre-defined protection.”

Let’s unpack those, starting with dynamic risk mitigation

“Within dynamic risk mitigation, the most recognizable products are risk control or volatility target indices. The notion behind these is simple: a dynamic allocation between risk-on and risk-off components, based on the prevailing market volatility, to meet a pre-determined target level.

In bullish conditions, the equity component participates in gains — often with leverage. When volatility picks up, the allocation shifts toward the risk-free asset to limit drawdowns.

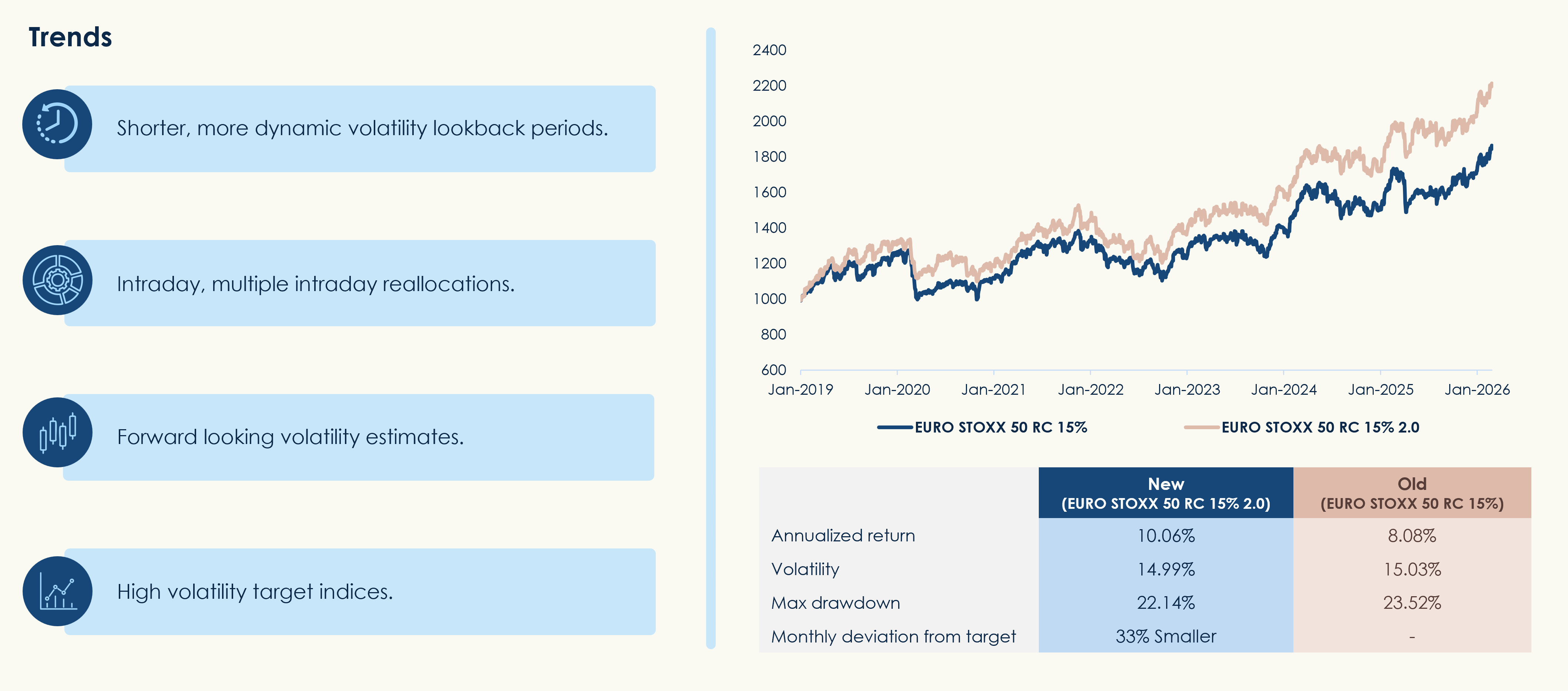

These products have become more sophisticated over time. Historically, the allocation mechanism relied on longer-term volatility lookback periods — 20, 60 or even 120 days — which performed well in hitting the volatility target but were slow to react. By shortening that lookback to 3, 5 or 7 days, and optimizing the leverage factor, we see clear improvements in performance, drawdown and deviation from the target, simply due to faster responsiveness.

The market has gone further still — intraday volatility target indices now exist with multiple intraday reallocations implemented via exchange-traded derivatives. The advent of weekly, daily and zero-day-to-expiry options has also enabled more dynamic, accurate, forward-looking volatility inputs to be incorporated into the allocation mechanism. Research shows that an increase in the accuracy of volatility measurements leads to a pick-up in performance.

These indices have seen their use expand beyond low-risk insurance products, with some now targeting higher volatilities than the underlying benchmark. They can employ leverage in order to reach volatility levels in the 30% to 40% range, producing accelerated returns in bullish markets, while still de-leveraging in times of market stress. This allows issuers to offer products with more attractive coupons.”

Figure 1: Volatility target indices

What about dynamic diversification?

“Dynamic diversification strategies have been particularly popular, with a number of products — often issued by banks — offering exposure across asset classes and regions. Global equity, fixed income and commodities, combined with dynamic allocation, allow these indices to react, diversify and mitigate risk. Beyond traditional asset classes, this diversification has also been seen between equity and volatility directly. A good example is the EURO STOXX 50® Volatility Balanced index, which allocates between the EURO STOXX 50 and short-term VSTOXX futures depending on the prevailing volatility regime, harnessing the well-known negative correlation between equity performance and volatility. It performed very strongly during the initial COVID-19 period (Figure 2), and more broadly in times of severe market stress.

There are also a lot of interesting rotation strategies in this space, using technical, sentiment and macroeconomic signals to drive systematic allocation. With the adoption of AI, the number of available indicators is growing, and we expect further expansion here.”

Figure 2: EURO STOXX 50 Volatility Balanced index – Performance

That leads us to pre-defined protection strategies. Can you walk us through those?

“In indexing, pre-defined protection has emerged primarily through defined outcome strategies — an area that has grown significantly since 2020. Assets under management in defined outcome ETFs in the US may reach USD 650 billion by 2030, up from USD 5 billion in 2019, according to BlackRock.[1]

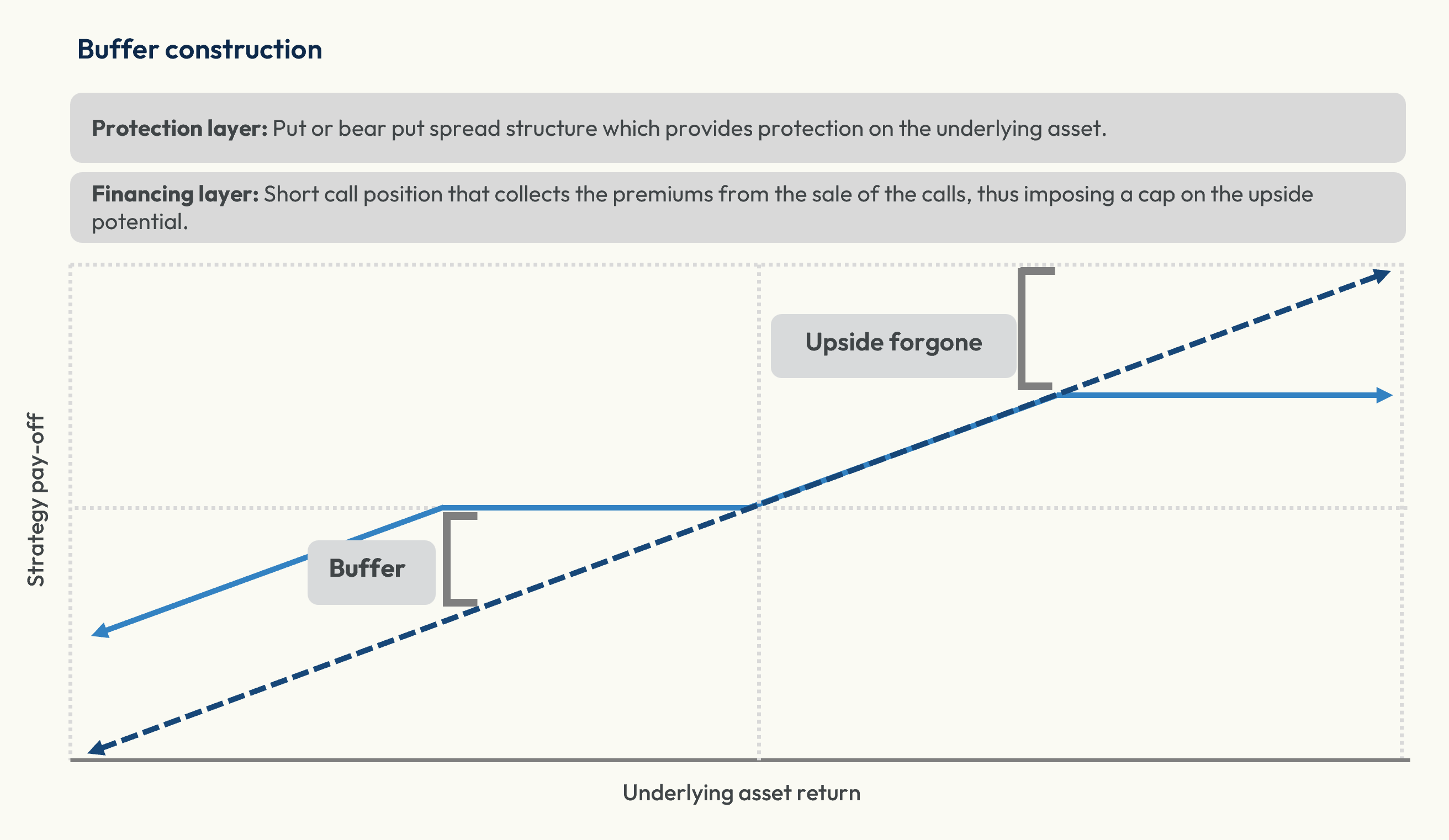

Early adaptations focused on protective put-like strategies, but these have been overtaken by buffer indices, particularly in the US. Buffer strategies closely resemble a put spread collar: long the underlying, a long near-at-the-money put, a short out-of-the-money put, and a short call. The result is downside protection up to a pre-defined buffer — typically between 5% and 20% — with any losses beyond that point reduced by that percentage (Figure 3). Upside participation is retained but capped, as the price for the protection and the zero-cost structure.

Buffer indices are not too complicated by design, but they were once out of reach for the retail investor. The combination of option positions would have made replication tricky, but combining them into one index, which can be wrapped into a single financial product, has now made them very accessible.”

Figure 3: Buffer indices

What strategies within this segment are seeing the most traction?

“Customization is king. Tailored buffer levels — shallow or deep — laddered buffers, volatility-based dynamic buffers and even strategies targeting 100% principal protection are all coming to market. End clients are no longer satisfied with off-the-shelf products; they want solutions precisely matched to their needs.”

These strategies are often used to underlie structured products. How do the two worlds connect?

“Volatility target and dynamic allocation strategies are commonly used as underlyings for structured products. But the influence runs both ways — defined outcome strategies have themselves taken direct inspiration from structured product payoffs. What we see in the structured product market often acts as a precursor to what later appears in the ETF market.

We are now seeing a real focus on pay-off design, with a number of indices based on structured products, either directly or through synthetic replication coming to market.

The clearest current example is autocallable-based indices, which have shown strong early traction. Similar research is ongoing around other structured products, such as Barrier Reverse Convertibles (BRC)-type structures. Now, in structured product terms both offerings sit in the yield enhancement category rather than pure capital protection — but in stable, moderate market environments the barriers in a BRC can provide meaningful downside protection while generating significant income. In larger market shocks, of course, that protection may not be sufficient, and that’s where pure capital protection products come in.”

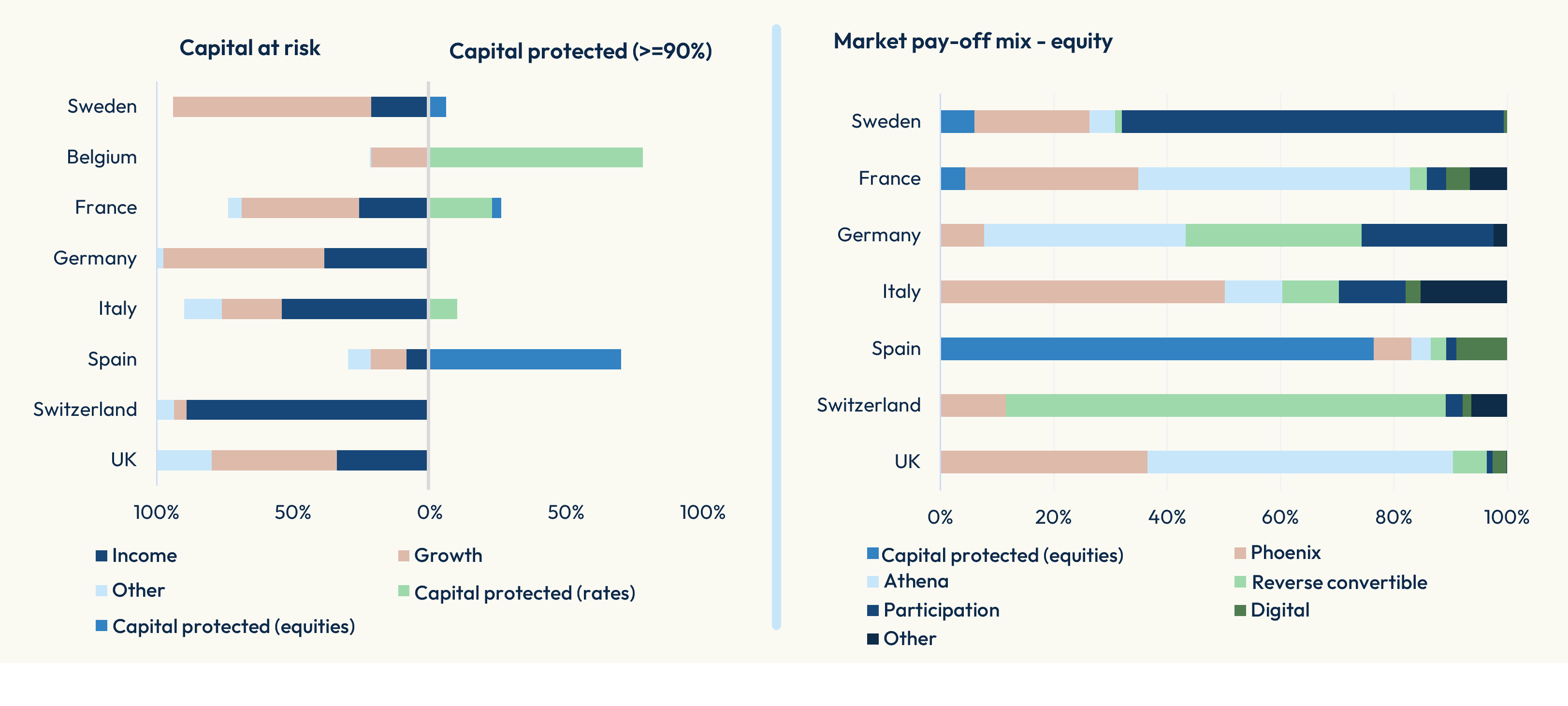

Capital protection products are used very differently across Europe. Can you explain that disparity?

“It would be misleading to talk about ‘the European structured product market’ as a single environment — it varies considerably by country. In Sweden, around 70% of issuance is uncapped growth and participation products. In Spain and Belgium, on the other hand, over 70% of products have built-in capital protection. Then you have Switzerland and Italy, where yield-enhancement products dominate. Even the underlying assets differ markedly: Sweden favours single-stock underlyings, the UK skews heavily toward index-linked products, and in Belgium around 80% of issuances are rate-linked.”

Figure 4: European structured product market

What does that tell us about the role structured products play more broadly?

“This differentiation is a real strength of the asset class — it shows structured products can serve any investment rationale, from protection to income generation to accelerated growth. They’ve moved from a niche, institution-focused category to something that is becoming mainstream and could now be seen as a prerequisite in the investor toolkit.

Since 2020, shifting stock-bond correlations, geopolitical uncertainty, pandemic and bubble fears have all underlined the necessity of protection. With necessity comes innovation, and strategy sophistication has evolved alongside the financial literacy of the retail investor. And the underlying demand is growing too. Driven by digital platforms, policy initiatives and low real returns on cash, we are seeing double-digit percentage growth in the number of retail investors across areas in Europe.”

How have index providers and product issuers responded to that growing client base?

“In indexing, products have become more complex and more tailored, but also more widely marketable. In structured products, the focus has been the opposite: simplicity, robustness and efficiency rather than over-engineered complexity. Together, that has opened up accessibility to a previously niche asset class.”

So where does all this lead? What are the key trends you’re watching across the offerings discussed?

“I’d highlight three. The first is AI adoption — we’re already seeing it used in the research, testing and validation of quantitative strategies, increasing efficiency across the value chain and creating more room for original thinking. It’s a significant opportunity for those willing to seize it.

The second and third trends may sound contradictory: standardization and customization. Standardization will come from the democratization of QIS and structured product investing — structured product ETFs are now available through standard broker accounts, customized QIS products have migrated from OTC to exchange-listed solutions, and I expect that to continue.

At the same time, more sophisticated investors want products precisely customized to their risk appetite, particularly around long-term, protected investing. De-risking and retirement-oriented investing is increasingly pervasive — or perhaps that’s just my interest changing as I get older! And at the other end of the spectrum, younger investors may gravitate toward higher volatility target indices or barrier-based structured products — still with an element of downside protection, but with a much more risk-on approach.

Whatever direction things move, there will be significant opportunities for all market participants.”

[1] BlackRock, “Outcome ETFs – A powerful tool for a changing world,” March 27, 2025.